The Surprising Answer That Sets This Insurer Apart

Most people choose an insurance company based on coverage options, price, and reputation—but few stop to ask who actually owns the company? That question is more important than it seems.

Ownership can impact everything: how claims are handled, how profits are used, and how much your voice matters as a customer. One insurer that stands out in this regard is Amica—a company often praised for customer satisfaction and loyalty. But who really owns Amica Insurance Company?

Let’s dive into Amica’s ownership structure, its impact on policyholders, and what sets it apart from the rest of the insurance industry.

A Quick Snapshot of Amica Insurance

Before we break down ownership, here’s a quick background:

Founded

1907 (Lincoln, Rhode Island)

Full Name

Automobile Mutual Insurance Company of America

Current HQ

Lincoln, RI

Core Products

Auto, Homeowners, Renters, Life, Umbrella

Customer Base

Over 1 million policyholders nationwide

Financial Strength

A+ rating from A.M. Best

Now onto the big question…

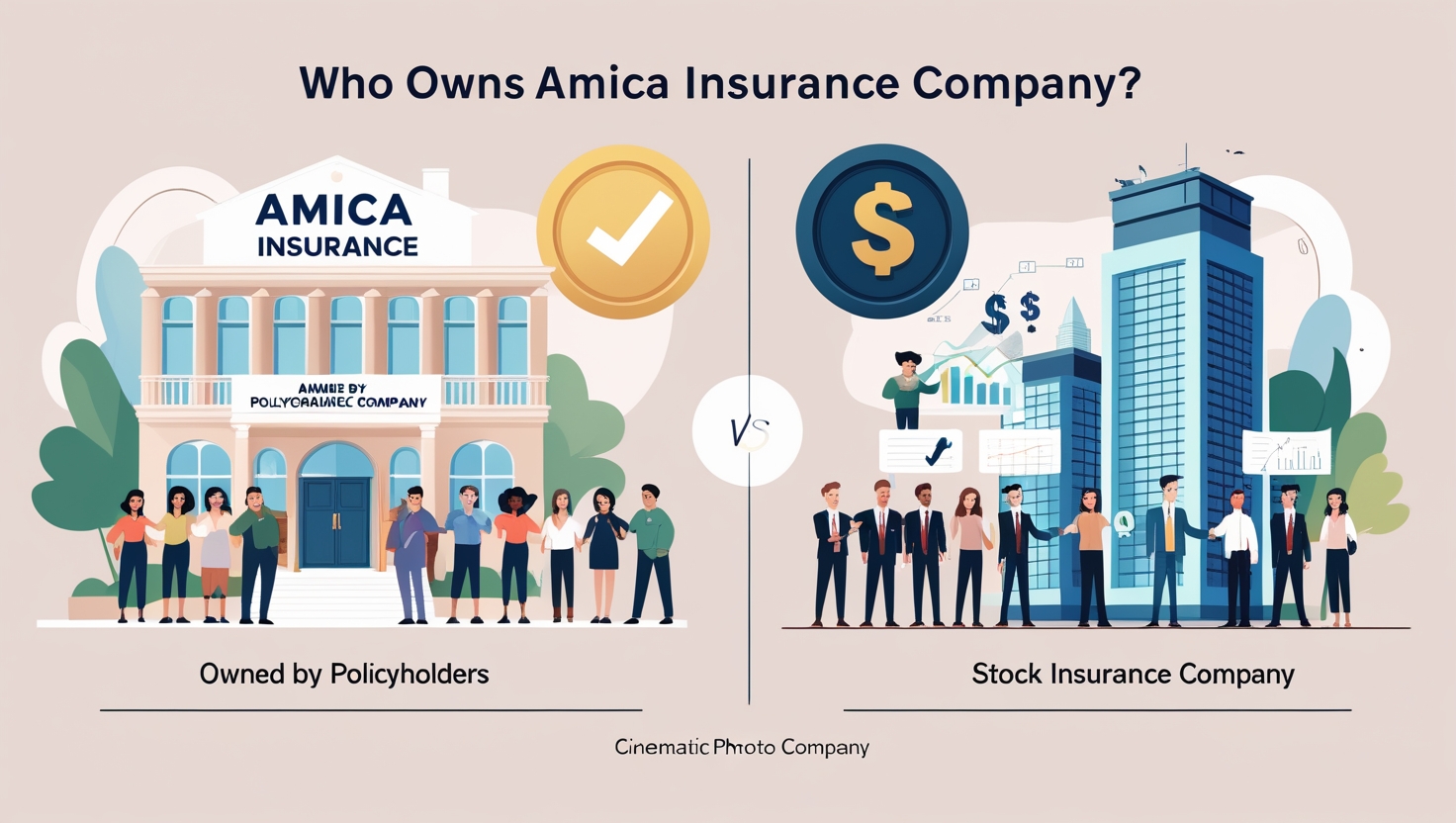

So, Who Owns Amica Insurance Company?

Amica is a mutual insurance company. That means it is owned entirely by its policyholders.

Yes, you read that right—Amica customers are its owners. There are no stockholders, no private investors, and no Wall Street pressure to boost quarterly earnings at your expense.

This mutual model is rare in today’s corporate-heavy financial landscape. But it’s at the heart of what makes Amica different—and arguably, better—for many customers.

What Does It Mean to Be a Mutual Insurance Company?

In simple terms:

Stock insurance companies are owned by shareholders, and their main priority is profit.

Mutual insurance companies are owned by policyholders, and their main priority is service and long-term value.

Here’s How It Plays Out in Real Life:

Aspect

Stock Company

Mutual Company (Amica)

Ownership

Shareholders

Policyholders

Profit Use

Dividends to investors

Reinvested or returned to policyholders

Accountability

Investors

You (the insured)

Decision Drivers

Share price & earnings

Customer satisfaction & stability

Amica’s model aligns the company’s success with yours. When the company does well, you benefit—often through dividends, lower premiums, or improved services.

Why Is This Ownership Structure So Rare?

Most big insurance companies in the U.S. are publicly traded. Think Allstate, Progressive, or Travelers. Going public gives companies quick access to capital for expansion, but it often shifts the focus toward investor returns over customer care.

In contrast, Amica has remained independent and mutual for over 100 years. That’s a deliberate choice—one that prioritizes long-term trust and policyholder satisfaction over short-term profit.

“We answer only to our policyholders, not shareholders. That lets us focus entirely on doing what’s best for them.” — Amica spokesperson, as quoted in Insurance Journal

Real-World Benefits of Amica’s Ownership Model

1. Consistently High Customer Satisfaction

Amica regularly tops customer service rankings. For example:

Ranked #1 in J.D. Power’s Auto Insurance Satisfaction Study multiple years in a row.

Consistently earns high marks from Consumer Reports for claim satisfaction and service quality.

This isn’t a coincidence—it’s a direct result of the ownership model. Amica doesn’t have to cut corners or rush claims to meet shareholder demands. Their loyalty lies with you.

2. Policyholder Dividends

Amica offers dividend policies on certain products—meaning you could receive part of your premium back if the company has a profitable year.

This is extremely rare in modern insurance. And it’s not just pennies—many policyholders report getting back 5% to 20% of their premiums annually.

3. Long-Term Thinking

Because Amica doesn’t answer to Wall Street, it can make long-term decisions—like investing in customer service, improving claims systems, or keeping rates stable—even when short-term profits dip.

Is Amica’s Mutual Structure Always Better?

Not necessarily. While mutual companies like Amica offer compelling benefits, they might not always be the best fit for every situation.

Here are a few considerations:

Fewer aggressive discounts or bundling perks: Stock insurers sometimes have deeper marketing pockets.

Slower expansion: Amica may not be available in every region or offer every niche policy.

Dividend policies might cost more upfront: Though they can pay off later, the premium for dividend policies is usually higher.

But for many, these trade-offs are worth it for a company that treats them like an owner—not a number.

How Does Amica Compare to Other Mutual Insurers?

Amica isn’t the only mutual insurer out there, but it’s among the most respected.

Mutual Insurer

Focus

Customer Reputation

Amica

Auto, Home, Life

Exceptional (J.D. Power leader)

Nationwide

Broad Coverage

Strong, but more corporate

Liberty Mutual

Large-scale insurer

Mixed reviews, hybrid model

State Farm

Auto, Home

Strong regional presence

What makes Amica different? Its size and focus. It’s not the biggest, but it consistently outperforms the giants in personalized service and trust.

A Personal Perspective: Why I Switched to Amica

I used to be with a major stock insurer. I had no complaints—until I filed a claim. That’s when I realized how impersonal and bureaucratic it felt. The rep didn’t even seem familiar with my case. It was all about numbers.

When I switched to Amica, the tone shifted entirely. I had a dedicated agent. I got a dividend after the first year. And when I had a tree fall on my roof, the claims process was smooth, transparent, and handled with empathy.

I’m not saying Amica is perfect—but it’s a rare case where the company actually feels like it’s on your side.

Final Thoughts: Should You Choose a Mutual Insurer Like Amica?

If you value personalized service, long-term reliability, and the feeling of being more than just a customer, then Amica’s mutual ownership model is a strong reason to consider them.

They may not have Super Bowl commercials or flashy sponsorships, but what they do have is integrity—rooted in their unique ownership structure.

And in today’s chaotic insurance landscape, that kind of stability is worth a lot.

Quick Recap: Key Takeaways

📌 Who owns Amica Insurance? Its policyholders—Amica is a mutual insurance company.

📌 Why does that matter? It means the company works for you, not shareholders.

📌 What are the benefits? Better service, potential dividends, long-term focus.

📌 Any downsides? Fewer discounts, smaller scale, higher upfront costs on some policies.

Explore More Insurance Insights

Curious how other insurance companies stack up? Check out our other deep dives:

Your Turn: Have You Ever Used a Mutual Insurance Company?

Share your experiences with Amica—or any mutual insurer—in the comments below. Let’s keep the conversation going! And if you found this post helpful, feel free to share it or subscribe for more insider insights on the insurance industry.